Groupon Built a Brain

It’s happening. A two-sided marketplace, an AI engine, and a frequency lever worth $100M a turn.

Nothing here is investment advice.

It’s happening. For years the Groupon story was a projection — a broken brand, a new operator, a plan on a slide. This is no longer a projection. Management went on LinkedIn and described, in public, the exact engine I’ve been asking for: an AI “Brain” that personalizes the app for each user, on the logic that design is cheap now and the whole game is what sits behind it. The relaunch built on that Brain ships in Q3.

Groupon is my highest-conviction long and the activism is going (very) well.

A TWO-SIDED MARKETPLACE, MORE RELEVANT THAN EVER

Groupon is the oldest good idea in commerce. Consumers want to spend less, small businesses want to fill empty tables, chairs, and appointment slots, and Groupon matches the two. In an economy ground down by inflation and increasingly owned by a handful of megacorps, a nail salon or a taco spot struggles to convert paid ads into a new customer. GRPN 0.00%↑ is one of the only channels where they don’t have to gamble on a creative. Demand on one side, savings on the other — that’s worth more in 2026 than it was in 2011.

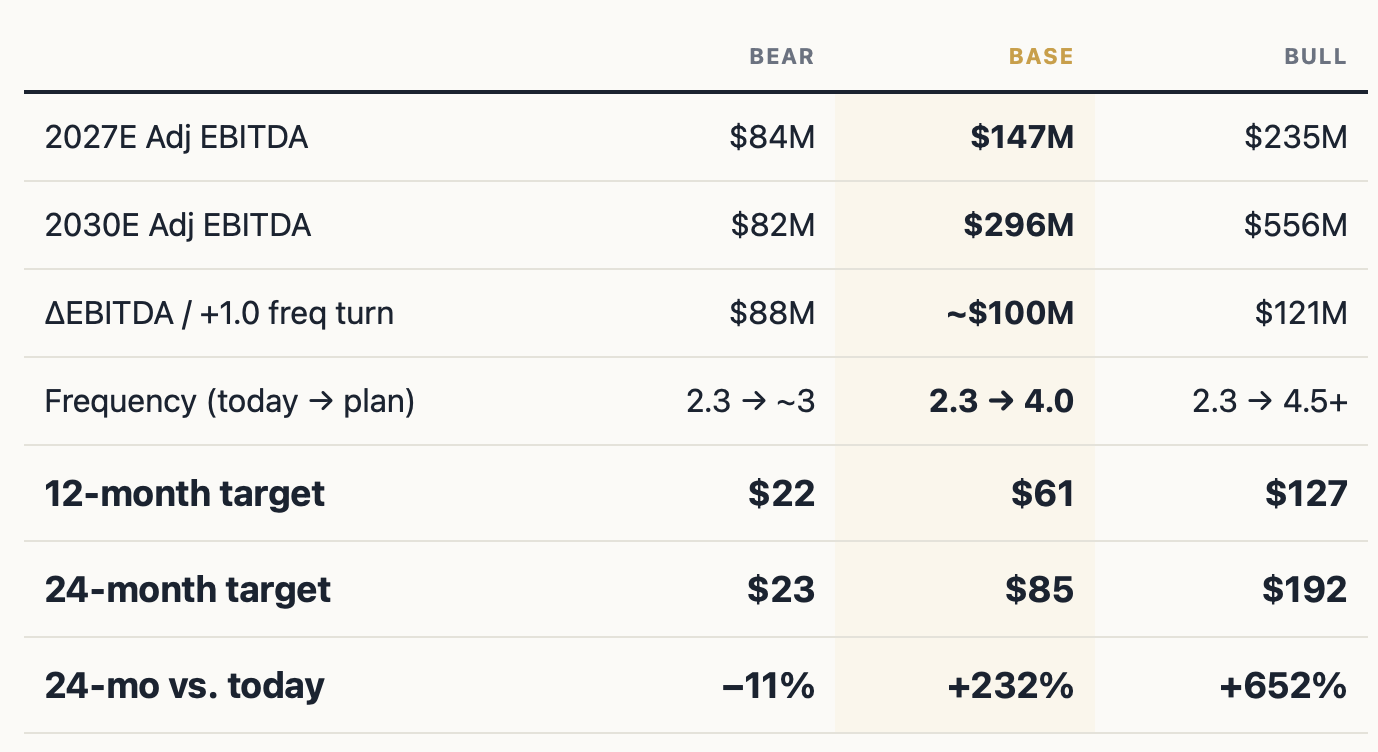

THE BRAIN IS A FREQUENCY MACHINE, AND FREQUENCY IS EVERYTHING

Groupon does not need more users. It needs the ones it has to come back more than twice a year. Frequency today is about 2.3 purchases per active user; my base case gets to 4.0. In the model, each turn is worth roughly $100M of EBITDA — more than the company earned in all of 2025. Personalization is how you move that number, and management just confirmed that is what they built and where they are aiming it.

The model assumes no acceleration in user growth. That is a real lever, and probably a large one, but it is too hard to forecast to underwrite, so every number below rests on frequency alone.

The Base case is a triple in two years and assumes no new-user growth at all — just frequency going from 2.3 to 4.0. The Bear case is roughly flat, because the buyback and the balance sheet catch the stock before the fundamentals do.

UGC AND GEN Z — THE UPSIDE I DON’T MODEL

That excluded user growth has an obvious place to come from. Groupon is a brand today’s under-25s barely know, which means it can become a new one for them. They live on short-form video and spend on experiences and small luxuries, and the way you reach them is user-generated content. Groupon has stood up a creator and influencer affiliate program, with creators posting real experiences that get tagged and tracked, the same approach that made a run of tired brands feel native on TikTok. If it works, it stacks on top of the frequency case instead of sitting inside it.

COSTS DOWN WHILE THE TOP LINE GROWS

The rare and valuable combination. Project Foundry is cutting headcount, and stock-based comp comes down with it, while billings reaccelerate. That is how a $69M EBITDA business becomes a $150M-to-$550M one without a heroic revenue line, with net margins heading toward 50% on a marketplace where the next transaction costs almost nothing to clear.

CAPITAL AND THE OPERATOR

Two more things underwrite the downside. Groupon owns ~1.79% of SumUp, the European payments company valued near $10B — roughly $180M to Groupon against a $75M cost. I’d sell it early, even at a discount, instead of waiting until 2027, but the stock should trade well in a market desperate for a growth stock. And the operator matters: Dusan Senkypl is a genuine technologist and turnaround specialist with major skin-in-the-game, and I think Groupon will be the biggest win of his career. He engages with shareholders, retail included, more than most teams bother to.

HOW TO PLAY IT

Owning shares lets you sleep. Calls into the Q2 beat (real-time data points to roughly $17–18M of EBITDA) and the Q3 relaunch carry the convexity. What would break it: North America billings decelerating hard or insiders at Pale Fire distributing rather than accumulating. Short of that, it’s happening.

See it yourself. Management’s walkthrough deck shows how the new experience actually looks. If you are in the US, download the Groupon app and run the new-user onboarding — that’s what opens the personalized version. The creator and UGC side is here.

Nick Nemeth runs Wyandanch Consulting LLC and publishes Mispriced Assets. The author holds a position in GRPN.

Have you notice, when you boil it down, everyone is selling time lately? GRPN is doing just that, glad to be in at $16!

Do you think they’ll need to hire back some of the AI layoffs? That might ding the margin picture.

Groupon is going to change the world of consumers. Again